We use cookies to understand how you use our site and to improve your experience.

This includes personalizing content and advertising.

By pressing "Accept All" or closing out of this banner, you consent to the use of all cookies and similar technologies and the sharing of information they collect with third parties.

You can reject marketing cookies by pressing "Deny Optional," but we still use essential, performance, and functional cookies.

In addition, whether you "Accept All," Deny Optional," click the X or otherwise continue to use the site, you accept our Privacy Policy and Terms of Service, revised from time to time.

You are being directed to ZacksTrade, a division of LBMZ Securities and licensed broker-dealer. ZacksTrade and Zacks.com are separate companies. The web link between the two companies is not a solicitation or offer to invest in a particular security or type of security. ZacksTrade does not endorse or adopt any particular investment strategy, any analyst opinion/rating/report or any approach to evaluating individual securities.

If you wish to go to ZacksTrade, click OK. If you do not, click Cancel.

SLF Stock Near 52-Week High: A Signal for Investors to Hold Tight?

Read MoreHide Full Article

Key Takeaways

{\"0\":\"Asset Management remains a priority, targeting higher ROE with lower volatility and strong upside potential.\\r\\n\",\"1\":\"Strong capital position supports steady dividend hikes and share buybacks.\\r\\n\",\"2\":\"Strategic shift to fee-based, capital-light businesses strengthens growth and stability.\\r\\n\"}

Sun Life Financial Inc. (SLF - Free Report) closed at $58.45 on Tuesday, near its 52-week high of $66.81. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

Shares have gained 5.6% in the past year compared with the industry’s growth of 5.7%.

Sun Life Financial has outperformed its peer, Reinsurance Group of America, Incorporated (RGA - Free Report) , which has lost 9.4% in the past year. Shares of Manulife Financial Corp (MFC - Free Report) and Primerica, Inc. (PRI - Free Report) have gained 11.6% and 8.7%, respectively, in the past year. With a market capitalization of $33.02 billion, the average number of shares traded in the last three months was 0.6 million.

SLF Shares are Expensive

Sun Life Financial shares are trading at a premium to the industry. The company’s price-to-earnings of 10.4X is higher than the industry average of 7.5X.

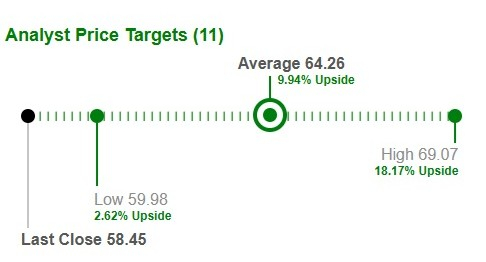

Target Price Reflects Potential Upside

Based on short-term price targets offered by 11 analysts, the Zacks average price target is $64.26 per share. The average indicates a potential 9.9% upside from the last closing price. Image Source: Zacks Investment Research

SLF’s Growth Projection Encourages

The Zacks Consensus Estimate for Sun Life’s 2025 earnings per share indicates a year-over-year increase of 9.6%. The consensus estimate for revenues is pegged at $27.03 billion, implying a year-over-year improvement of 16.1%.

The consensus estimate for 2026 earnings per share and revenues indicates an increase of 7.7% and 0.3%, respectively, from the corresponding 2025 estimates.

Optimist Analyst Sentiment on SLF

Two of the six analysts covering the stock have raised estimates for 2025 and 2026 over the past 60 days. Thus, the Zacks Consensus Estimate for 2025 and 2026 earnings has moved up 0.5% and 0.7%, respectively, in the past 60 days.

SLF’s Favorable Return on Capital

SLF’s return on equity (ROE) for the trailing 12 months is 17.2%, better than the industry average of 15.2%. This reflects SLF’s efficiency in utilizing shareholders’ funds. Underlying ROE continues to trend toward a medium-term financial objective of 18% plus, thus reflecting a sustained emphasis on capital-light businesses.

Key Points to Note for SLF

Sun Life Financial is focusing on the emerging economies of Asia, which are expected to provide higher returns and growth than the North American markets. It has a solid presence in China, the Philippines, India, Hong Kong and Indonesia and has also forayed into Malaysia and Vietnam. The contribution from the Asia business to SLF’s earnings has increased to 21% over the last few years.

Sun Life Financial envisions itself as one of the top five players and remains focused on growing its voluntary benefits business. The life insurer is also improving its business mix and shifting its growth focus toward products that require lower capital and offer more predictable earnings.

SLF has been working to strengthen Asset Management, which provides a higher ROE, requires lower capital, witnesses lesser volatility and has the potential for an earnings upside. Thus, Sun Life Investment Management’s investments in private fixed-income mortgages and real estate, as well as in pension plans and other institutional investors, should bear fruit.

Banking on its sturdy capital position, SLF distributes wealth to shareholders in the form of higher dividends and share buybacks.

Conclusion

The ongoing shift to fee-based capital-light businesses bodes well for growth. Operational efficiency has been aiding Sun Life in building a strong capital position. Consistent wealth distribution makes it an attractive pick for yield-seeking investors. Its dividend payout ratio is targeted within the 40-50% range.

Image: Bigstock

SLF Stock Near 52-Week High: A Signal for Investors to Hold Tight?

Key Takeaways

Sun Life Financial Inc. (SLF - Free Report) closed at $58.45 on Tuesday, near its 52-week high of $66.81. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

Shares have gained 5.6% in the past year compared with the industry’s growth of 5.7%.

Sun Life Financial has outperformed its peer, Reinsurance Group of America, Incorporated (RGA - Free Report) , which has lost 9.4% in the past year. Shares of Manulife Financial Corp (MFC - Free Report) and Primerica, Inc. (PRI - Free Report) have gained 11.6% and 8.7%, respectively, in the past year.

With a market capitalization of $33.02 billion, the average number of shares traded in the last three months was 0.6 million.

SLF Shares are Expensive

Sun Life Financial shares are trading at a premium to the industry. The company’s price-to-earnings of 10.4X is higher than the industry average of 7.5X.

Target Price Reflects Potential Upside

Based on short-term price targets offered by 11 analysts, the Zacks average price target is $64.26 per share. The average indicates a potential 9.9% upside from the last closing price.

Image Source: Zacks Investment Research

SLF’s Growth Projection Encourages

The Zacks Consensus Estimate for Sun Life’s 2025 earnings per share indicates a year-over-year increase of 9.6%. The consensus estimate for revenues is pegged at $27.03 billion, implying a year-over-year improvement of 16.1%.

The consensus estimate for 2026 earnings per share and revenues indicates an increase of 7.7% and 0.3%, respectively, from the corresponding 2025 estimates.

Optimist Analyst Sentiment on SLF

Two of the six analysts covering the stock have raised estimates for 2025 and 2026 over the past 60 days. Thus, the Zacks Consensus Estimate for 2025 and 2026 earnings has moved up 0.5% and 0.7%, respectively, in the past 60 days.

SLF’s Favorable Return on Capital

SLF’s return on equity (ROE) for the trailing 12 months is 17.2%, better than the industry average of 15.2%. This reflects SLF’s efficiency in utilizing shareholders’ funds. Underlying ROE continues to trend toward a medium-term financial objective of 18% plus, thus reflecting a sustained emphasis on capital-light businesses.

Key Points to Note for SLF

Sun Life Financial is focusing on the emerging economies of Asia, which are expected to provide higher returns and growth than the North American markets. It has a solid presence in China, the Philippines, India, Hong Kong and Indonesia and has also forayed into Malaysia and Vietnam. The contribution from the Asia business to SLF’s earnings has increased to 21% over the last few years.

Sun Life Financial envisions itself as one of the top five players and remains focused on growing its voluntary benefits business. The life insurer is also improving its business mix and shifting its growth focus toward products that require lower capital and offer more predictable earnings.

SLF has been working to strengthen Asset Management, which provides a higher ROE, requires lower capital, witnesses lesser volatility and has the potential for an earnings upside. Thus, Sun Life Investment Management’s investments in private fixed-income mortgages and real estate, as well as in pension plans and other institutional investors, should bear fruit.

Banking on its sturdy capital position, SLF distributes wealth to shareholders in the form of higher dividends and share buybacks.

Conclusion

The ongoing shift to fee-based capital-light businesses bodes well for growth. Operational efficiency has been aiding Sun Life in building a strong capital position. Consistent wealth distribution makes it an attractive pick for yield-seeking investors. Its dividend payout ratio is targeted within the 40-50% range.

Given the premium valuation, investors should wait for a better entry point for this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.